Lockbox vs. Electronic Lockbox: What’s the Difference?

Businesses today have more ways than ever to receive payments. Customers can mail checks, initiate payments through their bank's online banking bill...

4 min read

Businesses today have more ways than ever to receive payments. Customers can mail checks, initiate payments through their bank's online banking bill...

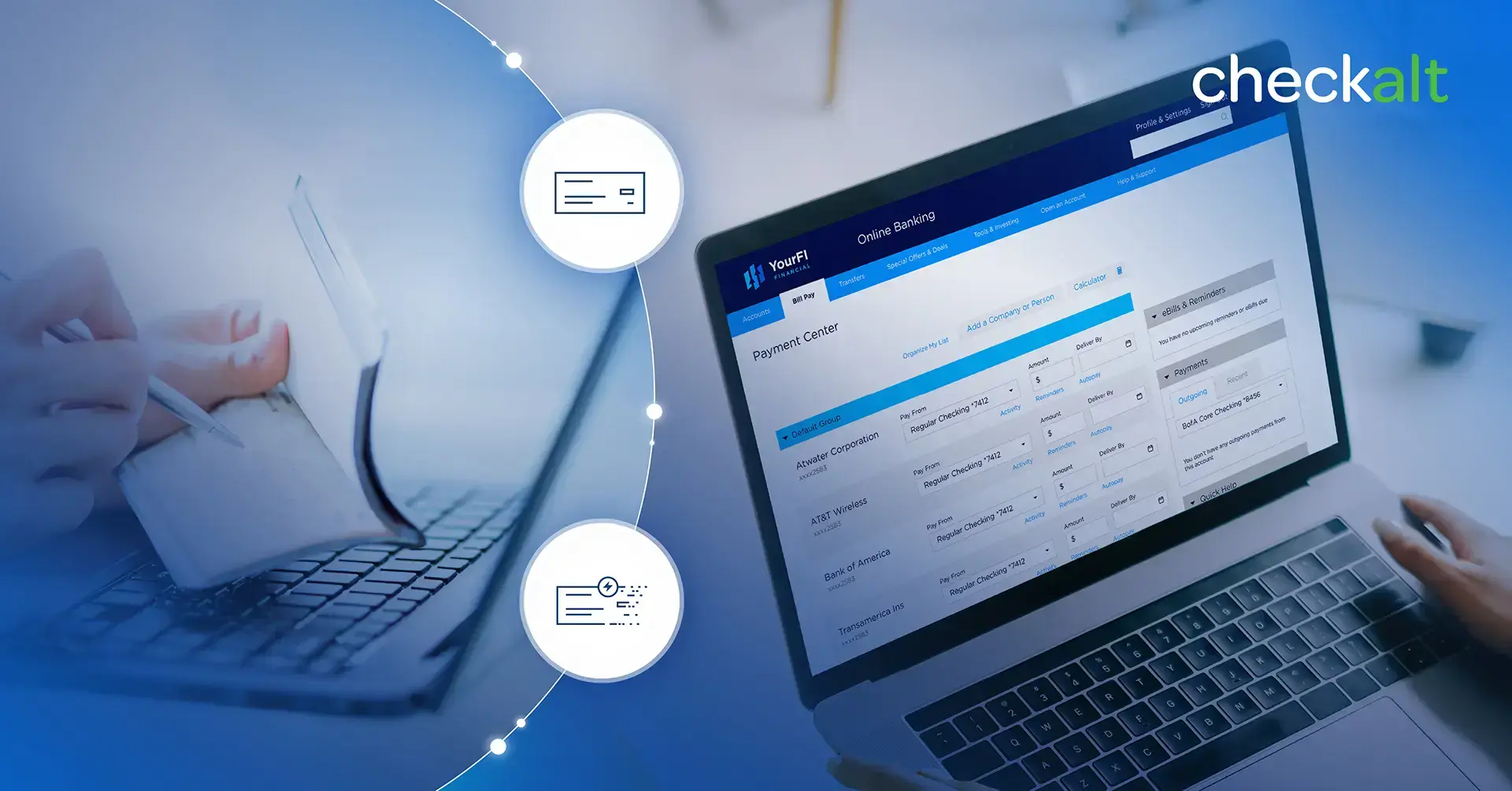

When a consumer uses their bank or credit union's online banking bill pay service, the experience feels entirely electronic. They log in, search for...

Lockbox services have been a cornerstone of receivables processing for decades, helping organizations streamline the collection and processing of...